“If you've been playing poker for half an hour and you still don't know who the patsy is, you're the patsy.”

Warren Buffet

I can’t claim to be a good poker player. I know how to play and have a good time when I do, but I know I am what my brother—a professional poker player—calls a “fish,” i.e., a bad player that pros can take advantage of.

However, what makes a fish a fish is that the fish doesn’t know he is a fish. That’s a lot of fish in one sentence. I know. This month’s newsletter is dedicated to a few fish that are slowly realizing they are the fish at the table.

Those of you who have been avidly reading my newsletter know the core of my thesis on fiat currency debasement. If you need a refresher, read any of the newsletters I have published this year (The Unstoppable Rise of AI and Outside Money, The Great Rug Pull, The Most Important Chart in the World, etc.)

Bond investors are one group that is waking up to the fact that they are the fish at the table.

A bond is a type of debt instrument that pays a fixed coupon and where investors usually receive the repayment of the principal at maturity. Since the coupon is fixed, they better hope inflation doesn’t accelerate or interest rates don’t rise.

In the first case, it means they won’t be able to keep up with inflation. In the second case, it means that the price of their bonds will fall, as prices will adjust to offer the yield demanded by the market despite the fixed coupon. This mechanism led to Silicon Valley’s collapse last year (see the newsletter I wrote on this for a more detailed explanation here). I am digressing, but I thought this little detour was necessary for what comes next.

As you know, central banks have started cutting rates, which should be good news for bond investors. Right?

In reality, the first 0.5 percentage point rate cut by the Federal led to an increase in long-term interest rates by 0.7 percentage points! With high deficits and no political will to cut spending on either side in the US, bond investors are looking around and realizing they are the fish at the table.

The chart below shows the performance of TLT, and Exchange Traded Fund (ETF) that invests in long-term US treasuries, compared to the S&P 500, Gold, and Bitcoin since the beginning of the year. It doesn’t get more fishy than that.

With bonds, investors get the worst of both worlds: they bear the full risk of fiat currency debasement and get a fixed coupon that is unlikely to keep up with inflation. If investors feel they are not adequately compensated for the risk they take by lending to fiscally irresponsible governments, the value of bonds will continue to drop.

US Treasury Secretary Janet Yellen knows investors don’t want the long-term bonds she sells. So, earlier this year, she decided to shift the issuance of US Treasuries to the front end of the curve. In plain English, she is borrowing short-term money because investors want to be able to get their cash out quickly in case the fiscal situation continues to deteriorate. This is a strategy similar to what many governments in emerging markets face: they issue short-term debt because investors are not willing to take any long-term risk on the value of the currency or the level of interest rates.

Another collateral damage: home buyers. Since the Fed cut, mortgage rates have skyrocketed in the US.

Paul Tudor Jones, the famous billionaire hedge fund manager, went on CNBC to explain that he was long gold, long Bitcoin, and owned no bonds. His thesis is that “all roads lead to inflation.” See the video below.

Everywhere you look, you see all-time highs:

When everything is at an all-time high, the issue may not be on the numerator side but on the denominator, i.e., the fiat currency in which these assets are denominated.

So what to do? Long story short: there are no great options.

How about gold? The sanctions imposed by the US and Europe on Russia’s foreign exchange reserves seem to have been the match that lit gold on fire. Central banks have been buying gold like there is no tomorrow ever since.

Gold has had an incredible run this year, but the main question remains: how much of the future money-printing has already been priced in? If you haven’t read it yet, you can read the newsletter I wrote on gold a few months ago here.

If you are interested in reading more about the topic of bonds and what alternatives investors should consider, I recommend the following recently released podcast episode: Thoughtful Money with Adam Taggart Luke Gromen: Bonds Are Now “Un-investable”

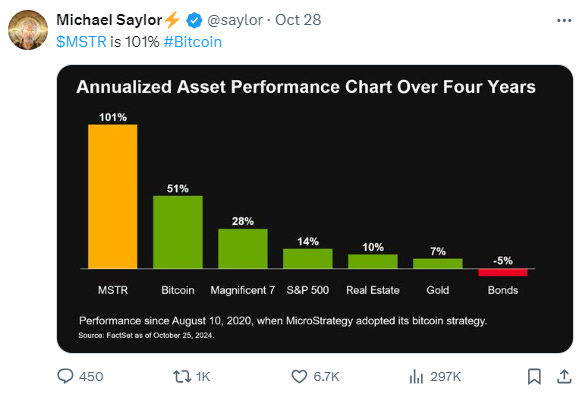

One company that has no doubt about what to do is MicroStrategy. This week, its chairman and Bitcoin billionaire, Michael Saylor, announced a 3-year plan to raise $42 billion to buy more Bitcoin!

The $21 billion At The Market (ATM) equity offering is nothing short of the largest in history. A few years ago, Tesla’s $5 billion ATM offering was considered massive.

At-the-market offerings are a type of follow-on public offering where a company sells newly issued shares into the market at prevailing prices, rather than at a fixed price as in a traditional IPO. ATM offerings allow companies to raise capital over time by selling shares gradually into the existing trading market.

Perplexity AI

Four years ago, MicroStrategy’s market capitalization was $1 billion. Then, Michael Saylor discovered Bitcoin, and MicroStrategy used all kinds of financial instruments to raise financing to buy as much Bitcoin as he could with it.

Today, MicroStrategy’s market capitalization is above $50 billion, a 50x increase. MicroStrategy borrowed to acquire some of its Bitcoin, so Saylor created a way for regular investors to buy Bitcoin with cheap leverage. Since MicroStrategy started acquiring Bitcoin in August 2020, its annualized return has beaten pretty much everything, including Bitcoin.

Now, let me throw in a plot twist: the value of MicroStrategy’s Bitcoin is “only” about $17 billion, not $50 billion. This dislocation between the market capitalization of MicroStrategy and that of its Bitcoin holding has led to hedge funds putting in place short positions on MicroStrategy and long positions on Bitcoin, hoping that the value of MicroStrategy would fall and converge toward that of its Bitcoin holdings. But the opposite happened. The spread between MicroStrategy and the value of its Bitcoin holdings has continued to widen. Billions of dollars have been lost by betting against MicroStrategy.

How is MicroStrategy defying the laws of finance and valuation? Because MicroStrategy is a darling of retail investors, so much so that its stock is traded more than that of Amazon or Google, which have market capitalizations 40 times bigger, and it’s risky to play against the retail crowd…

Those who think they can outsmart the market should remember the motto of the WallStreetBets sub-Reddit crowd: “We can stay retarded longer than you can stay solvent.” This is who they are up against.

Ignoring the mindset of retail investors led to the demise of Melvin Capital Capital a few years ago (see the newsletter I wrote about the GameStop saga here). Still, history seems to rhyme once again.

If you have made it this far into the newsletter, it means you’re really into chart porn, so let me throw another one at you: since August 2020, MicroStrategy has even outperformed Nvidia.

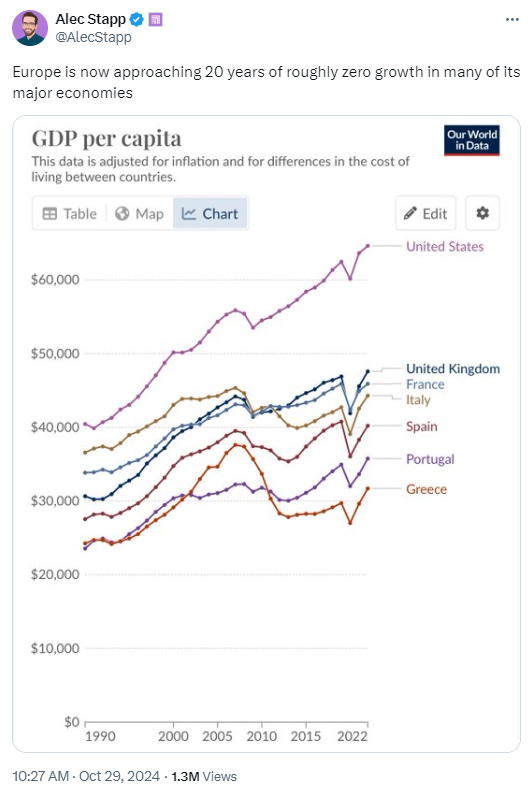

Bonus: Europe, the Ultimate Fish

Before the MicroStrategy $42 billion ATM offering derailed my plans to write about Europe, I thought I would write about the sad state of affairs there. It's hard to find a bright spot between anemic growth, overregulation, public finances, and high energy costs.

In 2008, the Eurozone's GDP was broadly equal to that of the US. Since then, the US GDP has almost doubled, while the Eurozone's has stagnated.

Stocks in Europe have gone nowhere, while their American counterparts have skyrocketed, led by the Magnificent 7.

Europe quickly imposed sanctions on Russia, particularly on its oil, but then it realized it still needed oil. India was very happy to oblige and provide all the oil Europe needed.

Spoiler alert: India’s oil production is tiny, so the oil comes from elsewhere…

While American companies like OpenAI and Anthropic are revolutionizing work with products like ChatGPT and Claude, the European Union passed the Artificial Intelligence Act earlier this year. This legislation was the world's first comprehensive legal framework designed to govern the use of AI systems. Fantastic. How about attracting talent so they can build AI companies first before deterring everyone with new regulations?

There may still be time for Europe to turn things around, but the solutions won’t be painless. Both Mario Draghi, the former head of the Europe Central Bank, and the IMF recently published reports and recommendations on what the EU can do. But the EU will first have to realize it is the fish at the table and take stock of what went wrong over the past two decades.